400 Billion Reasons To Believe In Brain-Computer Interfaces

Big TAM. So What?

Morgan Stanley’s latest report pegs the BCI market at $400 billion in the US alone.

“Brain Computer Interface Primer: The Next Big MedTech Opportunity?” by the bank’s equity analysts provides timely research, signaling to investors that this emerging frontier holds potential to generate substantial returns in future decades.

Note: As of publishing this article, Morgan Stanley’s 37-page report appears unlinked to a dedicated url, but the PDF has been circulating the commercial corridors of neurotech networks. This article is not the report. If you are unable to access the file, just reach out.

Major Takeaways

In addition to a brief summary of BCI’s origins and commercial history, the report covers key topics related to medical device outlook and ends with some speculation about the more distant future of this technology. But in a word, it’s about the TAM.

Investors and commercial leaders should understand the rationale behind the Total Attainable Market before they choose to believe it or not. The assumptions and fine print driving the analysis are the GPS for navigating BCI investment today more than any singular estimate. Here’s what you need to know:

Timeline to Scale: The authors expect commercial activity (product launch + reimbursement) “in about 5 years.” Over the next decade they forecast about $1.5 billion cumulative revenue, after which revenue could reach an annual run rate of $500 million by 2036 and $1 billion by 2041. But even by 2045, their models suggest market penetration will still only be 2.8%, meaning any “hockey stick curve” won’t occur for another 20 years.

Segmentation: Against their estimate of “nearly 10 million potential BCI candidates in the US,” they slice this into an a) early TAM, and b) intermediate TAM.

Early TAM - $80.8 billion: At least 2.8 million patients in the US, consisting of people with “critical upper limb impairment” as well as conditions like epilepsy and depression. The authors suggest these people will be first adopters of BCI.

Intermediate TAM - $320 billion: An additional 6.8 million people who have “moderate upper limb impairment and severe lower limb impairment,” will be the follow-on adopters, who opt for BCI once the technology is proven out in above applications.

8 Key Market Segments: ALS, Stroke, Spinal Cord Injury, Cerebral Palsy, Multiple Sclerosis, Limb Amputation, Epilepsy and Depression are identified as key indications where BCI would see uptake. More detail below.

Companies Mentioned: Synchron, Neuralink, Paradromics, and Precision are featured in the report, while Motif, CorTec and InBrain Neuroelectronics also get a mention.

Growth Drivers: Demographic trends, shifting norms, regulatory reforms and medical acceptance through emergence of clinical outcomes assessments and practice guidelines will slowly build traction. After BCI becomes established at a 1% penetration rate about a decade from now, the growth of clinical data, favorable insurance coverage, industry traction, and other factors could accelerate adoption.

Monetizing Medical Devices

An important caveat: Topline estimates only captures “potential revenue from a single implant procedure, ignoring a potential replacement cycle and likely recurring revenues from software.”

Curiously, while they cross-reference their BCI estimates against other implanted neurotech markets like “spinal cord stimulation ($2bn annual run rate), sacral neuromodulation ($1bn annual run rate), and hypoglossal nerve stimulation ($800mn annual run rate),” they leave out deep brain stimulation from their comparisons.

Sidebar: I suspect this was not an oversight, but rather an attempt to avoid undermining their own bullish outlook by analyzing an implanted brain device that has failed to cross $2b in run rate; as Schalk et al wrote earlier this year, “30 years after the introduction of DBS, only less than 3% of patients with Parkinson disease receive a DBS implant.”

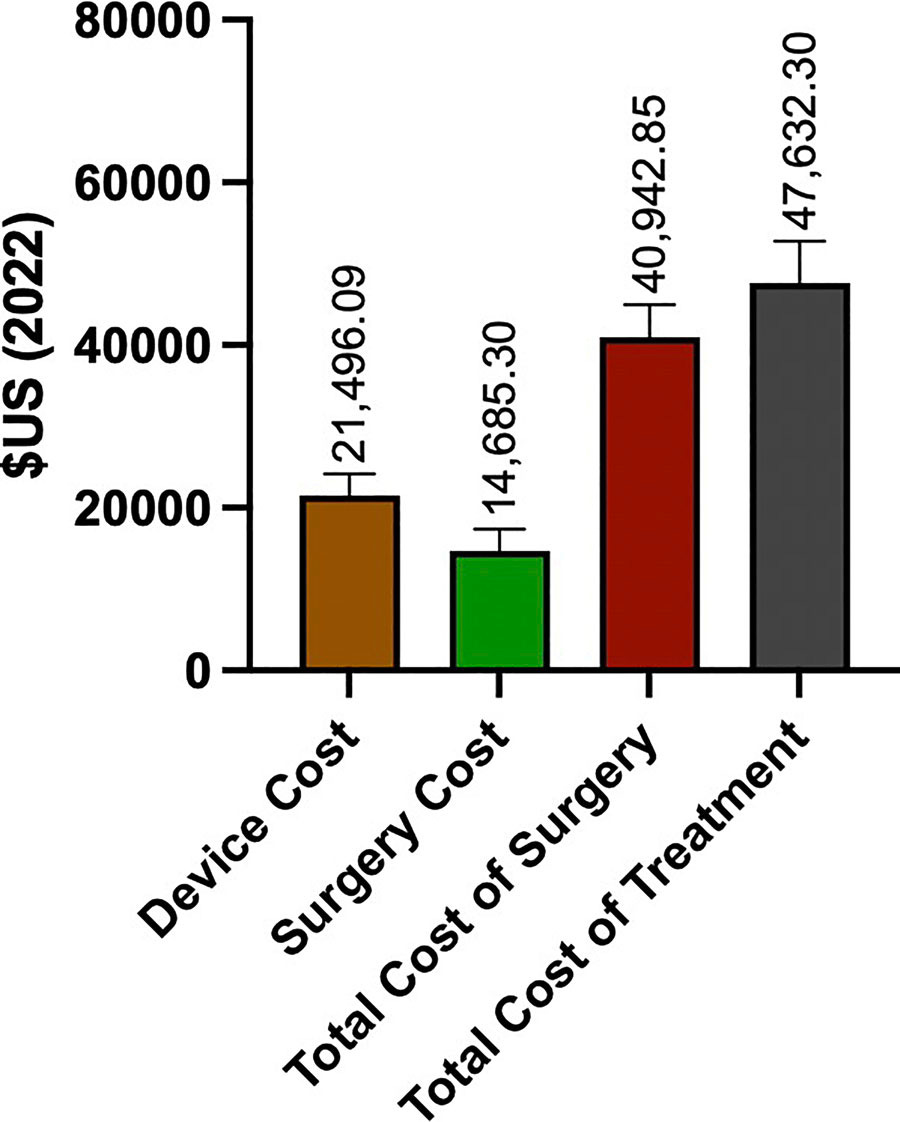

For sake of understanding this close proxy market however, I dug up recent average US DBS costs from Bishay et al’s 2024 Review.

In that paper, the chart to the left is followed by another chart that reveals how DBS costs vary by indication, from Parkinson’s to Essential Tremor or Dystonia. This variability underscores that no medical device is a monolith, and hints at the complexity of neurotechnology pricing and reimbursement strategy.

BCI costs will prove highly heterogeneous, between incomparable device designs, surgical approaches, clinical protocols, intended functionality, and much more. Morgan Stanley’s report reflects this across various market segment analyses, but the authors keep the math simple with a low tier and high tier pricepoint. Let’s dive in.

Humanizing the Market

Authors segment BCI into broad categories of product and market, and defining and sizing immediate and follow-on markets for each. There are some limitations inherent to any market research of this scope which we’ll touch on at the end.

While the Center for Medicare and Medicaid Services will need to determine appropriate coverage (reimbursement), they offer some ballpark estimates for sake of calculation:

Enabling BCIs - Estimated price $60k: Restore function and communication due to neurodegenerative diseases, stroke, or injury.

Preventative BCIs - Estimated price $30k: Mitigate or stop diseases or conditions such as depression to epilepsy. Initially, these may relay on existing codes for neurostimulation devices like those mentioned below, before new codes are approved.

The cross sections between “Enable/Prevent” and “Early/Intermediate,” makes the analysis a little byzantine, but the math really comes down to which people will have skin in the game.

Eight major market segments each feature an estimated population analysis that includes sizing rationale for both early-stage and intermediate-stage applications. A summary of the former suggests a near-term TAM of $80.8 billion (see above). The latter comprises a larger follow-on market opportunity worth up to $320 billion.

Some key assumptions and estimates behind the larger, intermediate TAM figures:

Motor Neuron Disease & Amyotrophic Lateral Sclerosis - $2.25 billion: Around 40,000 people in the US live with a MND, including 30,000 with ALS, with roughly 6,000 new diagnoses each year. Of this group, about 12,500 have critical upper limb impairment, representing an early BCI market, while about 25,000 people with “moderate upper and/or critical lower limb impairment” represent the follow-on market opportunity.

Stroke, Locked-In Syndrome - $48.6 billion : “There are less than 1,000 known cases of LIS in the US. There are roughly 900,000 strokes per year in the US, while 16% of these patients die, about a third of survivors will have a disability. We think about 5% of stroke cases result in a serious form of brain damage, which limits either speech or movement in a major way.”

Spinal Cord Injury - $10.8 billion: Around 300,000 people in the US are living with a traumatic spinal cord injury (SCI), with about 20,000 new cases occurring each year. Authors estimate about 45,000 of these patients who have severe upper limb impairment represent early BCI adopters. Longer term, BCI integrated with spinal cord stimulation could represent another 135,000 people. ONWARD is leading here, while Neuralink has mentioned animal models of spinal cord stimulation are in R&D.

As a note, the above three areas are fairly well established in the BCI industry, with Synchron, Neuralink, and Blackrock in active clinical trials, with Precision and Paradromics set to join them following FDA Breakthrough designations last year.

Multiple Sclerosis - $9.45 billion: Around 1 million people have MS, with about 7,000 new diagnoses each year. Morgan Stanley estimates about 7,500 of these folks would opt for a BCI.

Cerebral Palsy - $5.1 billion: Of the 500,000 adults in the US living with cerebral palsy today, about 5,000 have severe upper limb impairment, while about 80,000 live with moderate upper or severe lower limb impairment.

Limb Amputation - $4.5 billion: There's roughly 2.5 million people in the US living with limb loss, with an additional 180k requiring amputation each year. Approximately 40% are missing an upper limb (upper arm, forearm and hand), representing initial BCI adopters. Phantom Limb pain could represent a follow-on market here as well, with companies like Phantom and Bios developing solutions.

Epilepsy - $75 billion: About 3 million adults in the US suffer from epilepsy, with about 150,000 potentially eligible for a BCI to treat severe seizures in the short-term. Synchron has indicated interest in expanding here and Parkinson’s (which is mystifyingly absent from this report)

Depression - $242.5 billion : About 21 million people have depression, and about 2.5 million live with severe, treatment-resistant depression, representing the BCI opportunity here. The authors note this application would probably have a lower price point of around $25,000. Of the companies today, Motif is actively pursuing a solution here, and Medtronic DBS implants are also being explored.

While the authors suggest additional indications like ADHD, OCD, anxiety could become BCI markets, they stop short of scoping these opportunities in this analysis.

What vs So What

Beyond the above analysis, the report also explores eligible population growth projections, timelines for ramp up, penetration rates, and sales estimates on the early/intermediate rationale defined above for each condition.

It’s tidy yet squishy math that doesn’t summarize neatly. After spending a day poring through these numbers and a year studying this market, here are parting thoughts for executives keen on digesting this report to inform their go-to-market strategy in BCI.

Focus on 2030. The utility of 20-year economic models for a pre-commercial market analysis plateaus the further out you go; predicting revenue in 2045 for a group of companies that have not yet implanted a single human being is somewhat hollow. The numbers in this report seem eye-popping by design, but they represent the total attainable market. At the risk of offering basic advice: diligence on a company’s product/market fit, electrode design, read/write considerations, available clinical data, competition (from BCI, neurotech, pharma, digital health, and beyond) and economic evidence generation strategy for the next 5 years are a better use of your firm’s brainpower than guessing what Elon will be doing with Neuralink on Mars in his 70’s.

Understand Lead Indications. The report’s most salient analysis is the market segmentation, which can add real value to today’s discussions by creating a lingua franca of eligible patients. But what matters more today than refining guesstimates on average selling price and penetration rates, is understanding the unmet needs of populations living with neurodegenerative diseases, physical injuries, and psychiatric indications. BCI can certainly add value to people living with motor impairment, but the double- and triple-click into understanding costs and benefits alongside medications, caregivers, other assistive and digital technologies is the broader economic puzzle.

Do Your Own Research. Big numbers aside, there’s a lot missing in this report. Vision Restoration is not mentioned at all, despite at least three companies active there. Same with DBS and Parkinson’s, where InBRAIN’s FDA Breakthrough signals possible competition with Medtronic, Boston Scientific and Abbott as a potential “DBS 2.0.” I’m nitpicking, but the authors also mistakenly list Neurable’s EEG headphones as a BCI (it’s just not), while leaving out Axoft, Vonova and others that certainly are. Moreover, the panoply of implantable neurotechnologies might arguably be better investment opportunities with crossover potential into these same markets. For a report focused on long-term outlook, this is somewhat thin on the wealth of technologies, approaches, and rapid commercial R&D today.

Follow The Pioneers - The finance bros did a great job with the spreadsheet, but they don’t know it all, especially when it comes to technology’s role in living with disability. It’s stunning to me that this report doesn’t feature the word “Medicaid” once. Recent papers authored by Ian Burkhart, Jen French, and stalwart colleagues hold insights, recommendations, and boatloads of footnotes, data supplements, technical specs, and real-world implications for utilization, usability, product design and beyond. If you really want to understand the opportunity and challenge of serving this market, just start with stories like this one. I’d argue you’ll learn more about evaluating odds of market success than you will from the size of a TAM.

Originally published in Forbes on October 10, 2024.

Great analysis!